How Kam Financial & Realty, Inc. can Save You Time, Stress, and Money.

How Kam Financial & Realty, Inc. can Save You Time, Stress, and Money.

Blog Article

Top Guidelines Of Kam Financial & Realty, Inc.

Table of ContentsKam Financial & Realty, Inc. Can Be Fun For EveryoneAn Unbiased View of Kam Financial & Realty, Inc.Kam Financial & Realty, Inc. Fundamentals ExplainedAbout Kam Financial & Realty, Inc.Some Known Details About Kam Financial & Realty, Inc. What Does Kam Financial & Realty, Inc. Mean?Kam Financial & Realty, Inc. - The FactsEverything about Kam Financial & Realty, Inc.

If your regional county tax obligation rate is 1%, you'll be billed a residential property tax of $1,400 per yearor a month-to-month real estate tax of $116. Finally. We get on the last leg of PITI: insurance policy. Look, everyone that acquires a home needs home owner's insurance coverageno ifs, ands, or buts regarding it. That's not always a bad point.What an alleviation! Keep in mind that great, elegant escrow account you had with your residential or commercial property tax obligations? Well, think what? It's back. Just like your residential or commercial property tax obligations, you'll pay component of your property owner's insurance premium in addition to your principal and rate of interest payment. Your lending institution gathers those payments in an account, and at the end of the year, your insurance policy business will certainly draw all that cash when your insurance policy repayment is due.

The 9-Minute Rule for Kam Financial & Realty, Inc.

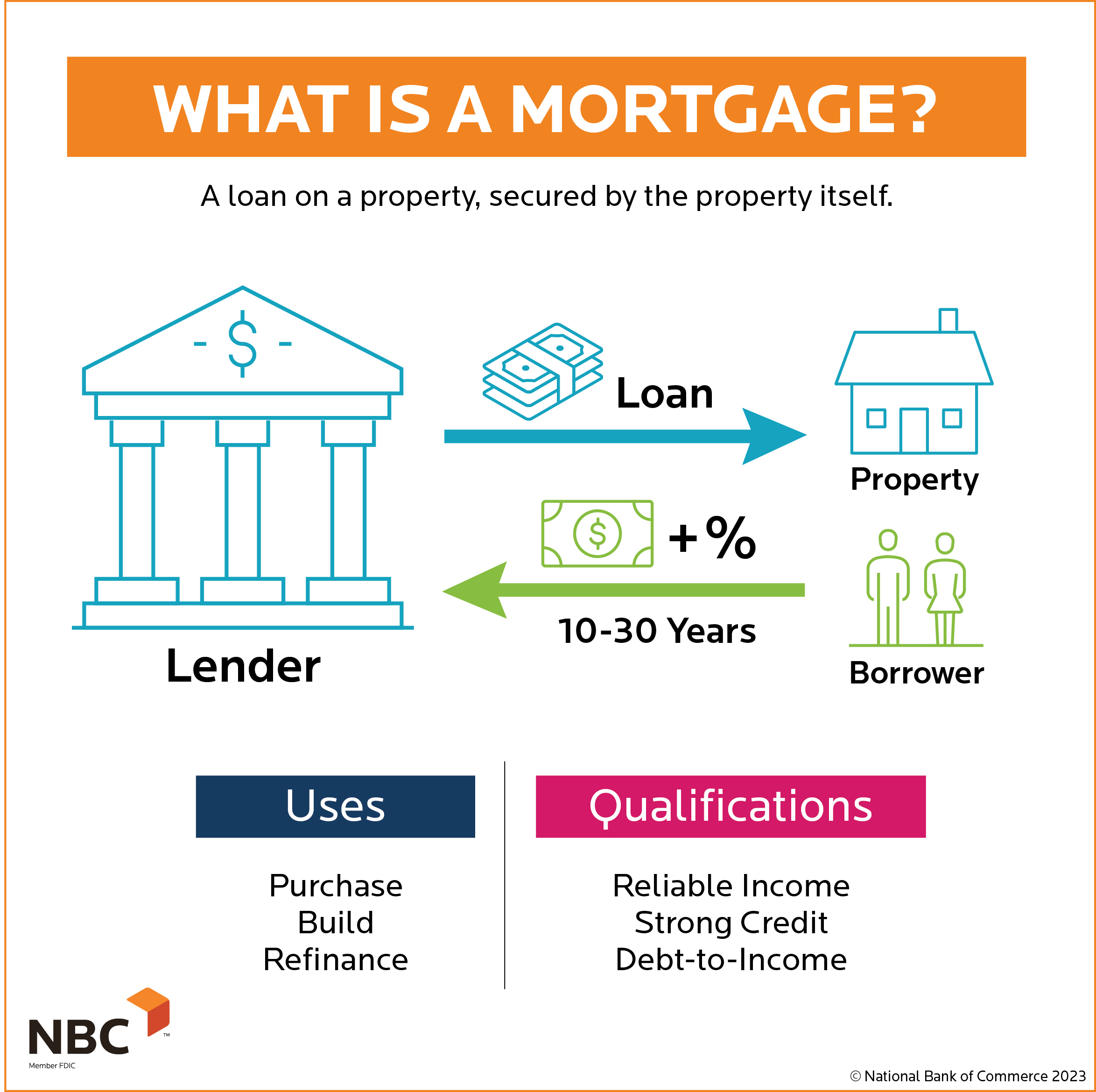

It's meant to safeguard the loan provider from youwell, a minimum of from the possibility that you can't, or just flat don't, make your mortgage payments. Naturally, that would certainly never ever be youbut the lender doesn't care. If your down repayment is less than 20% of the home's cost, you're going to get put with PMI.

If you come from an area like one of these, don't neglect your HOA fee. Depending upon the age and size of your house and the amenities, this can include anywhere from $50$350 to the quantity you pay each month for your overall housing prices. There are lots of kinds of home loans and they all charge various month-to-month repayment amounts.

The Of Kam Financial & Realty, Inc.

Given that you wish to get a mortgage the clever means, connect with our pals at Churchill Home loan - mortgage lenders california. They'll stroll with you every action of the means to place you on the very best course to homeownership

About Kam Financial & Realty, Inc.

This is the most typical kind of home funding. You can take a table lending with a set rate of rate of interest or a floating price.

A lot of lending institutions charge around $200 to $400. This is typically negotiable. mortgage loan officer california.: Table fundings give the technique of routine payments and a collection date when they will certainly be repaid. They use the assurance of knowing what your repayments will be, unless you have a floating price, in which situation settlement quantities can alter

10 Simple Techniques For Kam Financial & Realty, Inc.

Revolving credit scores car loans work like a large over-limit. Your pay goes right into the account and costs are paid of the account when they schedule. By keeping the loan as reduced as feasible at any type of time, you pay much less rate of interest since lenders calculate interest daily. You can make lump-sum repayments and redraw money as much as your restriction.

Application costs on revolving credit score home mortgage can be as much as $500. There can be a fee for the everyday banking purchases you do via the account.: If you're well organised, you can pay off your home loan much faster. This likewise matches individuals with uneven revenue as there are no fixed repayments.

Getting The Kam Financial & Realty, Inc. To Work

Deduct the financial savings from the total lending amount, and you just pay rate of interest on what's left. The more cash money you keep throughout your accounts from day to day, the a lot more you'll save, due to the fact that passion is computed daily. Connecting as many accounts as feasible whether from a companion, moms and dads, or various other family participants means also less rate of interest see post to pay.

The Ultimate Guide To Kam Financial & Realty, Inc.

Settlements start high, yet decrease (in a straight line) gradually. Charges resemble table loans.: We pay less rate of interest generally than with a table loan since very early repayments include a greater repayment of principal. These may fit customers that anticipate their income to go down, for instance, if one companion plans to give up job in a couple of years' time.

We pay the interest-only component of our repayments, not the principal, so the payments are lower. Some consumers take an interest-only loan for a year or more and after that switch over to a table funding. The regular table car loan application fees apply.: We have a lot more cash money for various other things, such as remodellings.

Kam Financial & Realty, Inc. - Questions

We will certainly still owe the total that we borrowed up until the interest-only period ends and we begin repaying the car loan.

The home loan note is normally taped in the public records along with the mortgage or the deed of trust and acts as proof of the lien on the property. The home mortgage note and the home loan or action of count on are 2 various files, and they both offer different legal objectives.

Report this page